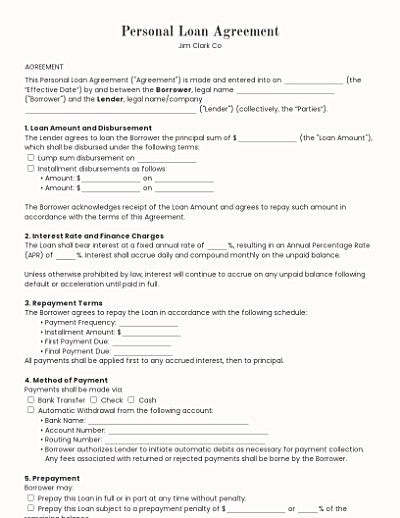

Personal Loan Contract

Jim Clark Co

Free Template

A personal loan agreement describes the terms for lending money between parties. It typically lists the principal amount, repayment schedule, interest format, and basic obligations connected to the loan arrangement.

Personal loans fall into two broad categories: secured and unsecured. A secured loan is tied to property that the lender relies on as collateral. An unsecured loan has no collateral requirement and relies on general borrower creditworthiness instead. A public-facing overview of these two structures often highlights how lenders assess risk, how repayment terms are arranged, and how the presence or absence of collateral impacts the agreement language. Borrowers commonly review these distinctions when comparing loan options.

Interest rate structure shapes the overall cost of a personal loan. A fixed rate stays the same throughout the term, while a variable rate may change based on external benchmarks. A personal loan agreement typically describes how the rate is set, when adjustments may occur, and how these adjustments influence periodic repayment amounts. Many users search for this topic because it directly affects long-term affordability and loan predictability.

Loan term length affects how long repayment extends and how much interest may accumulate. Shorter terms often lead to higher periodic payments, while longer terms spread out repayment over more time. Personal loan agreements commonly reference the chosen term, payment intervals, and the expected timeline for completing repayment. Users researching loan term length generally want a simple overview of how the duration impacts the total amount repaid without diving into legal interpretation.

Jim Clark Co

Jim Clark Co

This Personal Loan Agreement ("Agreement") is made and entered into on (the “Effective Date”) by and between the Borrower, legal name ("Borrower") and the Lender, legal name/company ("Lender") (collectively, the “Parties”).

1. Loan Amount and Disbursement

The Lender agrees to loan the Borrower the principal sum of $ (the "Loan Amount"), which shall be disbursed under the following terms:

Lump sum disbursement on

Installment disbursements as follows:

The Borrower acknowledges receipt of the Loan Amount and agrees to repay such amount in accordance with the terms of this Agreement.

2. Interest Rate and Finance Charges

The Loan shall bear interest at a fixed annual rate of %, resulting in an Annual Percentage Rate (APR) of %. Interest shall accrue daily and compound monthly on the unpaid balance.

Unless otherwise prohibited by law, interest will continue to accrue on any unpaid balance following default or acceleration until paid in full.

3. Repayment Terms

The Borrower agrees to repay the Loan in accordance with the following schedule:

All payments shall be applied first to any accrued interest, then to principal.

4. Method of Payment

Payments shall be made via:

Bank Transfer Check Cash

Automatic Withdrawal from the following account:

5. Prepayment

Borrower may:

Prepay this Loan in full or in part at any time without penalty.

Prepay this Loan subject to a prepayment penalty of $ or % of the remaining balance.

Any prepayment shall be first applied to accrued interest, then to the outstanding principal balance.

6. Security for the Loan (Collateral)

This is an unsecured loan.

This Loan is secured by the following collateral:

In the event of Borrower’s default, Lender shall have the right to take possession of and dispose of the collateral in a commercially reasonable manner, as permitted by law, to recover the balance due.

7. Late Fees and Default

If any scheduled payment is more than days late, the Borrower agrees to pay a late fee of $ or % of the overdue amount, whichever is greater. Failure to make two or more payments or any material breach of this Agreement shall constitute default.

In the event of default, the Lender may:

8. Modification of Terms

No provision of this Agreement may be amended, modified, or waived except in writing signed by both parties. Oral modifications shall be invalid and unenforceable.

9. Termination

This Agreement shall terminate upon the full repayment of the Loan and any accrued interest, or earlier as mutually agreed in writing by the parties.

Lender may terminate this Agreement upon Borrower’s default by written notice, and all unpaid obligations shall become immediately due and payable.

10. Entire Agreement

This document represents the entire agreement between the parties. It supersedes all prior discussions, negotiations, or representations. No other promises, conditions, or understandings shall be binding unless stated herein.

11. Severability

If any provision of this Agreement is deemed unlawful or unenforceable, such provision shall be severed, and the remaining provisions shall remain in full force and effect.

12. Governing Law and Dispute Resolution

This Agreement shall be governed and interpreted under the laws of the State of , without regard to its conflict-of-law provisions.

Any disputes arising under this Agreement shall be resolved by:

Mediation

Binding Arbitration

Civil Litigation in the courts of

The prevailing party in any legal proceeding shall be entitled to recover reasonable attorney's fees and court costs.

13. Signatures

By signing below, the parties acknowledge that they have read, understood, and agreed to the terms of this Agreement.

Answers to our most asked questions about personal loan agreement templates

Contact usDiscover more articles that align with your interests and keep exploring.