Auto Loan Contract

Jim Clark Co.

Free Template

Drive Deals with Confidence: Draft auto loan contracts to set expectations, outline payment terms, and ensure smooth financial transactions.

***

An Auto Loan Contract is a legal agreement between a lender and borrower that defines the loan amount, interest rate or APR, repayment schedule, fees and penalties, collateral (the vehicle), late payment consequences, and the borrower’s obligations in case of default.

***

A good auto loan contract lays out everything in black and white: how much is being borrowed (loan amount), the interest rate (like the price tag on the loan itself), how it will be paid back (repayment schedule), and what happens if things don't go according to plan (rights and obligations). This way, the borrower and the lender are on the same page from the get-go.

An auto loan contract is a three-way street:

Not all contracts are born equal! But some important bits are there to protect everyone involved. Let's take a peek at the clauses that should be paid attention to:

Ready to talk about repayments? Buckle up! Knowing the options is key to an easy ride for both the borrower and the lender. Here's a breakdown of the most common plans, their perks, and a few things to keep in mind.

This is the most common repayment option for car loans. It works like this: the borrower makes a set amount each month until they’ve paid off the loan in full. This payment covers a chunk of what they borrowed (principal) and the interest.

Paying bi-weekly is like paying half the rent every two weeks instead of once a month. With 52 weeks in a year, that adds up to 26 half-payments, basically squeezing in an extra full payment each year (13 instead of 12).

Some loan contracts let borrowers fast-track their way to freedom by paying off the loan early. They can do this by making a big one-time payment or by bumping up regular payments.

The best payment plan depends on the borrower's budget, payment style, and plans. Find a lender who explains all the options clearly, and pick the one that gets things cruising without blowing the budget.

Forget the paperwork headaches! Butterscotch has customizable templates that make drafting an auto loan contract a breeze. Here’s how it works:

That auto loan contract? It's not just something you skim and sign. It's the financial path to a new car! By understanding what's in there, the borrower can make sure they’re borrowing what they can afford, and the lender gets their money back. With Butterscotch, spend less time on paperwork and more time cruising in your new ride!

Jim Clark Co.

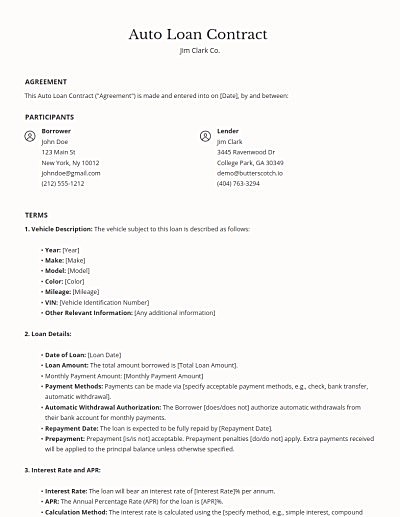

This Auto Loan Contract ("Agreement") is made and entered into on [Date], by and between:

1. Vehicle Description: The vehicle subject to this loan is described as follows:

2. Loan Details:

3. Interest Rate and APR:

4. Collateral: The vehicle described in Section 1 serves as collateral for this loan.

5. Acceleration Clause: In the event of missed payments or default, the lender reserves the right to demand immediate payment in full of the remaining loan balance. This clause may be enforced if the Borrower fails to make a payment within [specify grace period, e.g., 10 days] of the due date or breaches any material provision of this Agreement.

6. Amendments: This Agreement may be amended only by a written document signed by both parties. Any changes must be discussed and agreed upon by both parties before they take effect.

7. Termination:

8. Entire Agreement: This Agreement constitutes the entire agreement between the parties and supersedes all prior negotiations, representations, or agreements, whether written or oral.

9. Severability: If any provision of this Agreement is found to be invalid or unenforceable, the remaining provisions will continue to be valid and enforceable.

10. Dispute Resolution and Governing Law: Any disputes arising under this Agreement shall be resolved through the following procedures:

11. Signatures: By signing below, the parties agree to the terms and conditions outlined in this Auto Loan Contract.

This Agreement constitutes the entire agreement between the parties and supersedes all prior negotiations, representations, or agreements, whether written or oral. This Agreement may be executed in counterparts, each of which shall be deemed an original, but all of which together shall constitute one and the same instrument.

Answers to our most asked questions about auto loan contract templates

Contact usDiscover more articles that align with your interests and keep exploring.